How to Plan for Rising Health Care Costs in Retirement: The Power of HSAs

Planning for retirement? Don’t overlook the growing cost of health care. This post highlights how Health Savings Accounts (HSAs) can be a crucial tool in your financial strategy. HSAs offer unique tax benefits that can help you save and pay for medical expenses, both now and in the future. Learn how to maximize your HSA and protect your retirement savings.

Retirement and Rising Health Care Costs

The cost of health care continues to climb with no signs of slowing down, making it one of the most significant expenses in retirement. A 65-year-old retiring today could spend approximately $165,000 on health care throughout retirement, according to recent estimates – and that figure nearly doubles for couples.1 As Americans live longer, preparing for these expenses becomes an essential component of any comprehensive financial plan.

There are various approaches to addressing future health care costs including tax-advantaged savings accounts, Medicare supplemental insurance policies, long-term care insurance, and strategic retirement income planning. Each approach offers unique advantages depending on an individual’s health status, financial situation, and retirement timeline. Taking a multi-faceted approach that combines several of these strategies often provides the most comprehensive protection against escalating health care expenses.

In particular, Health Savings Accounts (HSAs) stand out as a helpful yet underutilized tool available to eligible individuals. Since their introduction in 2004, HSAs have evolved from a relatively unknown option to one of the more tax-advantaged vehicles in the financial planning landscape. HSAs are typically available only to those who have high deductible health care plans, but can dramatically improve both current tax situations and long-term financial security.

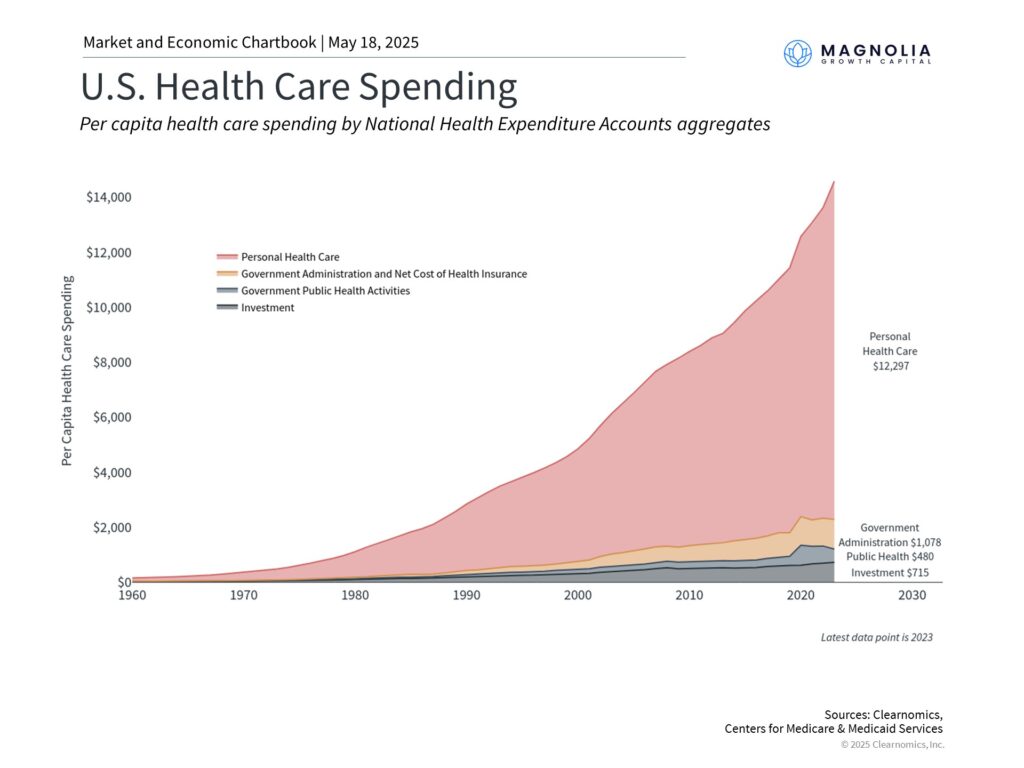

Health care costs continue to rise at an alarming rate

The growth in health care expenditures in the United States has been remarkable over the past several decades. In 2023, health care spending reached $4.9 trillion nationally – approximately $12,297 per person each year, and nearly 18% of GDP.2 This marks a dramatic increase from just 5% of GDP in 1962.

Multiple factors drive this persistent growth, including an aging population, rising prevalence of chronic conditions, advances in medical technology, broader insurance coverage, and overall health care cost inflation.

So, what financial planning strategies are available? This should be considered across three areas:

- Tax planning: Identifying strategies to fund health care expenses in a tax-advantaged manner, such as HSAs, and deciding whether to let these accounts grow in a tax-friendly way.

- Retirement planning: Understanding your future health care needs and determining the best funding vehicles. Again, HSAs can play an important role.

- Estate planning: In the event you don’t utilize your health care allocation, assessing how different vehicles like HSAs will be treated becomes a worthy consideration.

HSAs offer significant tax advantages with growing contribution limits

For those who qualify, HSAs are a valuable financial planning tool. HSAs are available to individuals enrolled in high-deductible health plans (HDHPs), which in 2026 means plans with minimum deductibles of $1,700 for individuals or $3,400 for families.3

What makes HSAs truly unique is their tax treatment. They are the only financial vehicle that offers triple tax advantages:

1. Tax-deductible contributions: Funds contributed to an HSA reduce your taxable income in the year of contribution, providing immediate tax savings.

2. Tax-free growth: Any interest, dividends, or capital gains earned within an HSA accumulate completely tax-free.

3. Tax-free withdrawals: When used for qualified medical expenses, withdrawals from HSAs are entirely tax-free, regardless of when they occur.

The combination of above tax benefits make HSAs mathematically superior to both traditional and Roth retirement accounts when the funds are used for qualifying health care expenses.

Contribution limits for HSAs have steadily increased over time. For 2026, the IRS allows contributions of up to $4,400 annually for individual coverage and $8,750 for family coverage, representing a 2.3% increase from the previous year. Individuals aged 55 and older can make an additional $1,000 in catch-up contributions annually. These contributions can come from you, your employer, or a combination, but cannot exceed the annual limits.

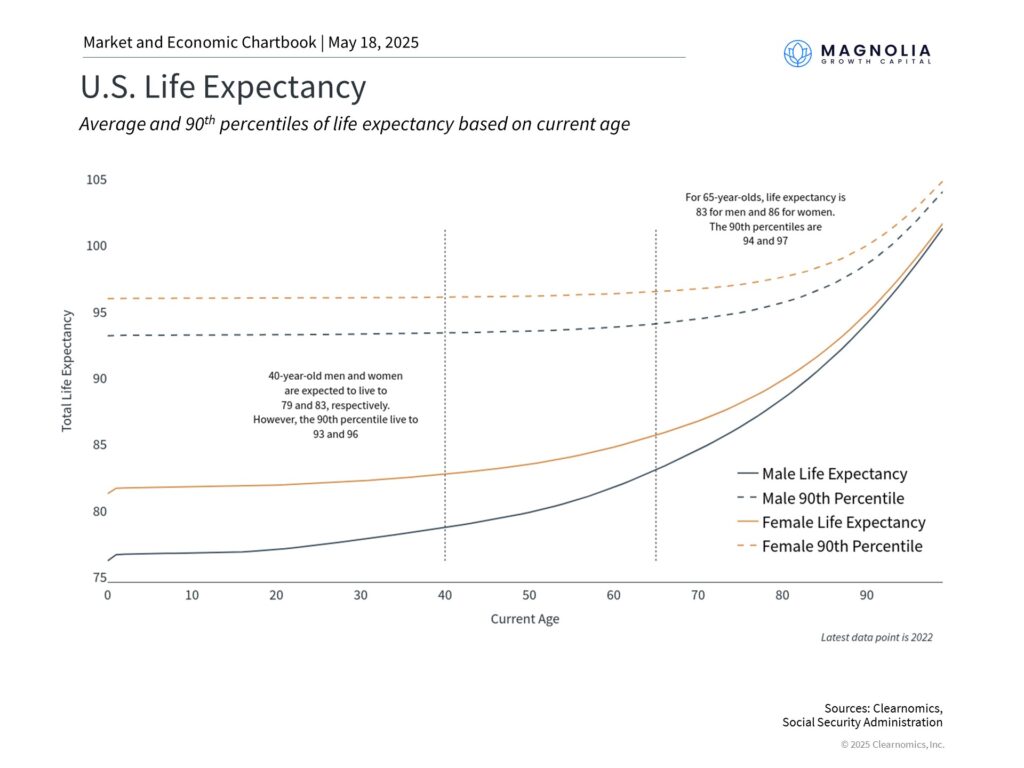

HSAs can transform retirement planning

With average life expectancies now extending well into the 80s for those over 65, the financial implications of extended retirement years have become increasingly significant, especially related to health care expenses.

One of the most advantageous HSA strategies – and one that many account holders overlook – is to treat your HSA as a specialized retirement account specifically for health care expenses. This approach involves maximizing annual HSA contributions while potentially paying some of your current medical expenses out-of-pocket. In this case, keeping receipts for qualified medical expenses you pay out-of-pocket is helpful, as these can be reimbursed from your HSA at any point in the future – even decades later – with no time limit.

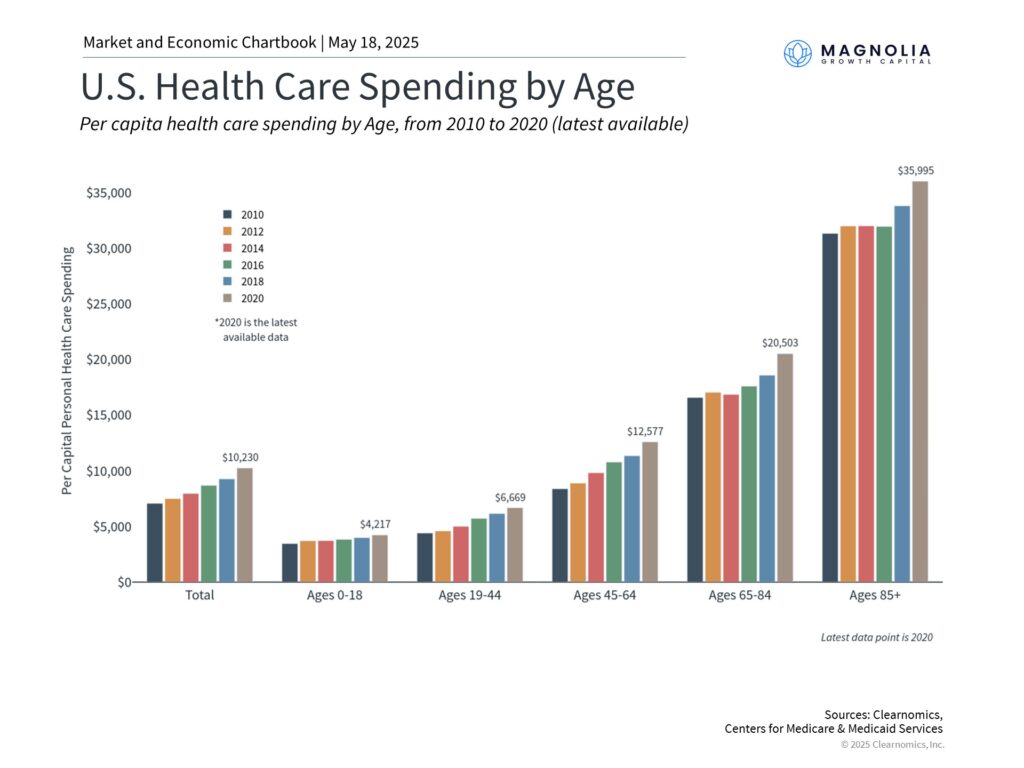

Health care costs are highest in retirement

The key to implementing this strategy is that HSA funds are invested for long-term growth – allowing HSA investments to gain tax-free over time. This is a critical step that many account holders miss, with most HSA providers offering various investment options. Over an extended time period, this can create a tax-advantaged reservoir specifically designated for retirement health care needs.

Unlike many retirement accounts, HSAs have no required minimum distributions during your lifetime, allowing for maximum tax-advantaged growth potential. Additionally, after age 65, HSAs become even more flexible, as the 20% penalty for non-health care withdrawals disappears. While non-qualified withdrawals would still be subject to ordinary income tax (similar to a traditional IRA or 401(k)), this flexibility makes HSAs particularly helpful for retirement planning.

HSAs can play a strategic role in estate planning

Beyond retirement planning, estate planning should be considered within your broader financial strategy. The treatment of HSA funds after death depends on the designated beneficiary, and can be a great way to carry forward the tax advantages to your spouse.

Specifically, if your spouse is the named beneficiary, the HSA transfers to them with all tax advantages intact. They can continue to use the account as their own HSA, maintaining all the triple tax benefits.

For non-spouse beneficiaries such as children or other individuals, the treatment is less favorable and can create a significant tax burden, especially if the HSA is sizable. In some situations, it may be more tax-efficient to name your estate as the beneficiary.

These estate planning considerations highlight the importance of integrating your health care funding strategy within your broader financial plan, ideally with guidance from a qualified financial advisor who understands both the tax implications and your personal circumstances.

The bottom line? Rising health care needs pose a significant financial planning opportunity. HSAs are a great tool for this purpose, with unmatched tax advantages for one of life’s largest expenses. For eligible individuals, HSAs are well worth incorporating into your financial planning strategy.

1. https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

2. https://www.ama-assn.org/about/ama-research/trends-health-care-spending

3. https://www.irs.gov/government-entities/federal-state-local-governments/where-can-i-learn-more-about-health-savings-accounts-hsa-and-health-reimbursement-arrangements-hra

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Magnolia Growth Capital LLC (referred to as “MGC”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute MGC’s judgement as of the date of this communication and are subject to change without notice. MGC does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall MGC be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if MGC or a MGC authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.

Investment strategy customization and risk management

Investment strategy customization and risk management